Church Bonds: The Bad and the Good

Church bonds sound like a great investment. They are a loan to a Church with two guarantees. The Church agrees to pay the loan back and to pay interest until the loan is repaid. If you are Christian, what better guarantee could you have? You are loaning money to other Christians with a guarantee that they will pay back the loan and pay you interest along the way.

Some Church bonds are reputable investments. However, the wholesome nature of Church bonds is one of the reasons that anyone considering them as investments should be highly critical of anyone offering them. Jesus warned us that business transactions of this world might not be what they appear to be. In the Parable of the Shrewd Manager, Jesus taught his disciples of a rich man that had a deceitful business manager. The business manager made deals for the rich man, and unbeknownst to the rich man, the business manager was taking an extra cut of profits without the rich man's knowledge.

Eventually, the rich man found out that his business manager was betraying his trust. The business manager was called before the rich man and asked to provide an account of all his business dealings, and then the business manager was to be dismissed. The business manager was more dishonest than the rich man thought. Rather than wrapping up his business transactions, the business manager contacted the people that he had business dealings with on behalf of the rich man. He told the people that he could settle their accounts with the rich man for half of what they owed. The business manager intended to keep all the proceeds from his transactions for himself.

The rich man found out that the business manager was betraying him once again and had the business manager brought to him. At this point, the parable takes an unexpected turn. Rather than being furious with the business manager, the rich man commended the business manager for his cleverness!

Jesus referred to the business manager as the "unjust steward." The lesson to be learned from this parable was a warning to the disciples. Jesus said, "The rich man had to admire the dishonest rascal for being so shrewd. And it is true that the children of this world are more shrewd in dealing with the world around them than are the children of the light" (Luke 16:8, NLT). The point that Jesus was making in this verse is that there are people in this world that will say or do whatever they can to take advantage of "the children of the light" or Christians.

When considering Church bonds or other types of investments, take Jesus' advice and be cautious because there are people in this world that will do whatever they can to take advantage of kind trusting people such as Christians. Regretfully, we see an example of what Jesus was teaching the disciples about in a case that recently occurred in Pigeon Forge, Tennessee. A man that became a pastor perpetrated a Ponzi scheme that solicited funds from his congregation for the "purchase of purported church bonds and claimed the funds would be used for the benefit of the church, particularly to pay off the church's debt" (Johnson, 2018). The pastor was arrested, tried and convicted in federal court of stealing from senior citizens. He was sentenced to more than five years in prison and ordered to pay his victims $1,373,361.96.

Church bonds from a good bond broker can be a worthy investment. Church members will often feel safe or obligated to buy Church bonds if their Church is issuing the bonds. If you have the financial capability to purchase Church bonds that are issued by your Church, then other than you making a straight gift, Church bonds can be an excellent way to help the Kingdom of God. Sometimes the Church bond is not the problem; it is the person selling the bond. One of the most common complaints about Church bonds is that they were misrepresented and inappropriate for certain investors.

If you do have an interest in purchasing Church bonds, here is how to gauge the legitimacy of the investment. There are two types of Church bonds, private placement bonds and registered bonds. To be a private placement investment, bonds must be offered to less than 35 people and total less than $5 million in face value. Even private placement Church bonds are required to have financial statements. If you are interested in a Church bond that is a private placement, ask for the bond's financial statements. If you do not understand financial statements, talk to a CPA or a financial advisor. Church bonds that are over the 35 investor limit or $5 million dollar value must register with the Securities and Exchange Commission, and the broker must register with a self-regulatory organization called FINRA. You should be able to request supporting documents from the SEC and FINRA to verify that the Church bond and the broker are legitimate.

If you are buying Church bonds as a significant part of your personal investments for your retirement or other investment goals, you should be very cautious. Church bonds will react like any other bond. When interest rates go up, the bond's value will go down and vice versa. When Church bonds are issued, their interest rates are tied to the economy so that they can be relatively competitive with other bond investments.

Church bonds have unique characteristics that can affect their ability to repay the bond. If a Church that is issuing bonds is in a community that is hit by high unemployment, the tithes and offerings to the Church will be directly affected. A Church's ability to repay a bond can also be affected by the Church's leadership. If there is a death, congregations may stop giving and that puts the ability to repay the bond in jeopardy. With every Church bond, it is important to inquire if there is a succession plan for the lead pastor which includes life insurance where the Church is named as the beneficiary. A succession plan could also cover any other circumstances from disability, to divorce or other situations that could lead to a scandal. There have also been instances where Churches have lost their tax-exempt statuses because of their activities. While interest earned on a Church bond is taxable, the loss of tax-exempt status of a Church will mean that donors to that Church will not have any tax-benefits from giving.

It does not take much searching on the internet to find examples of Church bond defaults. Church bonds have a number of market forces that can negatively affect their value. The market for Church bonds is tiny compared to the corporate bond market. In 2017 the annual amount in the United States that was spent on religious sector construction was about $3.5 billion (Rolfs, 2017). In August of 2018, the St. Louis Federal Reserve listed annual construction expenditures for the entire United States at over $1.3 trillion (FRED, 2018). That means that Church construction is about 2.7% of the nation's construction economy. Only a small portion of the 2.7% is in Church bonds. There are other types of competing Church loan programs such as commercial mortgages. That is why Church bonds rarely have ratings from rating services such as Moody's or Standard and Poors. They are too small. Church bonds usually have limited liquidity. If you buy a Church bond and want to redeem it before it matures, you may not be able to find a purchaser. Alternatively, to find a purchaser, you may need to reduce the selling price to an amount below the underlying market rates.

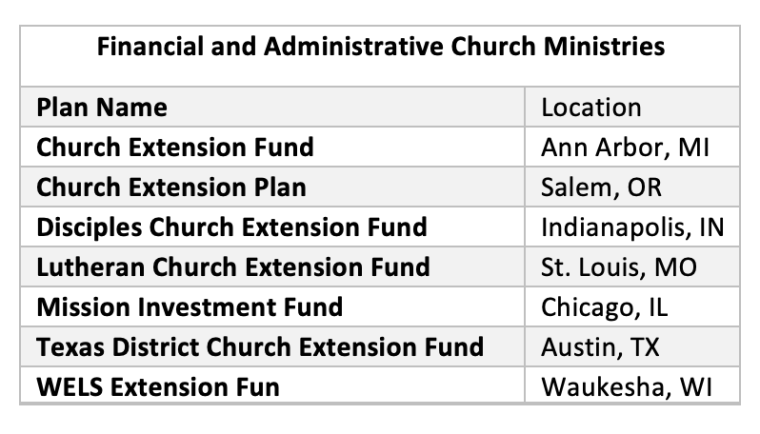

Alternatives to Church bonds for those wanting to invest in similar biblically responsible investments include Church-based financial service companies accepting investments much like banks and credit unions that offer interest-bearing accounts. These are organizations that are closely connected to certain Christian denominations and provide the services to their congregations a well as the general public. They bring in deposits and loan their assets to their Church community. Here is a short list of examples:

Finally, there are two critical questions for a Christian investor to consider when investing in Church-based securities. Is your priority to support a Church's mission by purchasing investments that are tied to the Church? Or, is your goal to satisfy your religious morals by investing in biblically responsible income-producing investments? Regardless of your choice, be a responsible Christian investor and be informed.

–Van Richards is a Christian financial advisor as well as the founder of https://www.Advice4LifeInsurance.com and http://www.Advice4Retirement.com. Van draws from his 30 years as a financial advisor to write about financial issues from a Christian perspective. You can contact him at van@advice4lifeinsurance.com.